Release-Date

Reference-Number

2025-0400-SR17

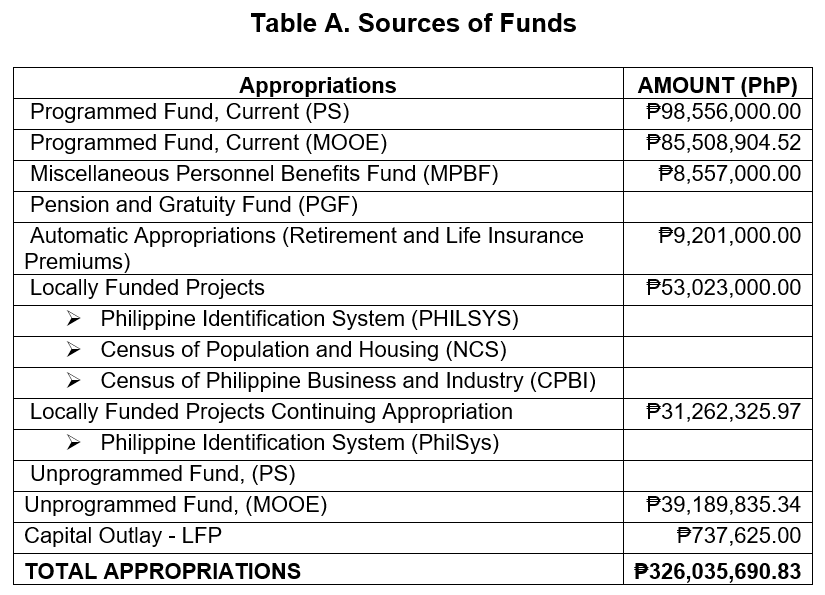

The PSA RSSO IV-A has been allocated with a total budget of approximately PhP326 million as of March 31, 2025. This is the amount of funding set aside for the office's operations, projects, and activities during the year. A total of PhP737 thousand was allocated specifically to Capital Outlay related to Generation/Compilation of Community-Based Statistics (CBSS). The remaining portion of the budget, PhP39.2 million or thirty-seven percent (37%) of the appropriations came from Unprogrammed Fund and Locally Funded Projects both Current and Continuing (MOOE) (refer to Table A).

The PSA RSSO IV-A has been allocated with a total budget of approximately PhP326 million as of March 31, 2025. This is the amount of funding set aside for the office's operations, projects, and activities during the year. A total of PhP737 thousand was allocated specifically to Capital Outlay related to Generation/Compilation of Community-Based Statistics (CBSS). The remaining portion of the budget, PhP39.2 million or thirty-seven percent (37%) of the appropriations came from Unprogrammed Fund and Locally Funded Projects both Current and Continuing (MOOE) (refer to Table A).

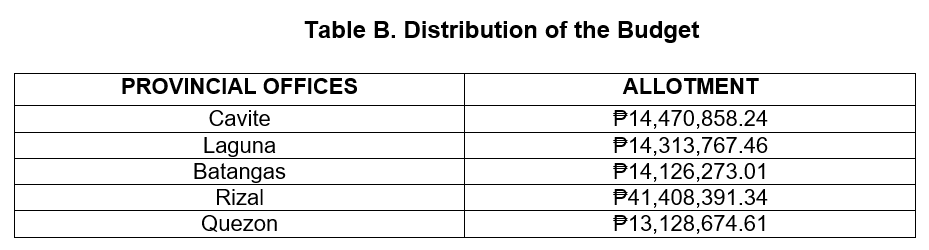

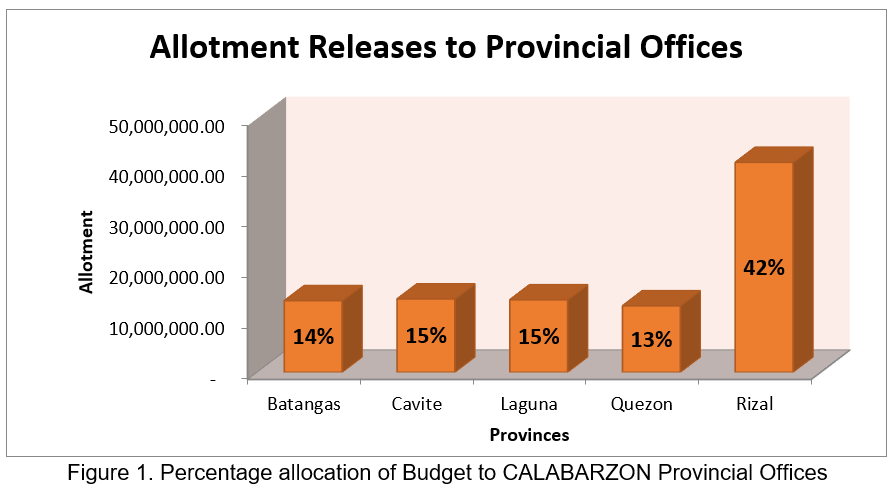

The sub-allotment release order to CALABARZON Provincial Offices as of March 2025 amounted to Php97 million which comprised 30% of the total allotment. The remaining 70% was at the Regional Statistical Services Office IV-A and part of it is still for distribution to the provincial office until December 2025. The funds allocated to the Provincial Offices are distributed unevenly across the provinces, depending on various factors such as population size, economic activity, and specific statistical needs of each province. The distribution is as follows, Rizal province received the highest share of the budget at 42%, or roughly Php41 million. On the other hand, Quezon received the lowest share corresponding to 13%, or around Php13 million of the total budget for the whole region. The distribution reflects the principle of equity in resource allocation, where the funding is allocated to different provinces based on their unique needs and circumstances (refer to Table B and Figure 1).

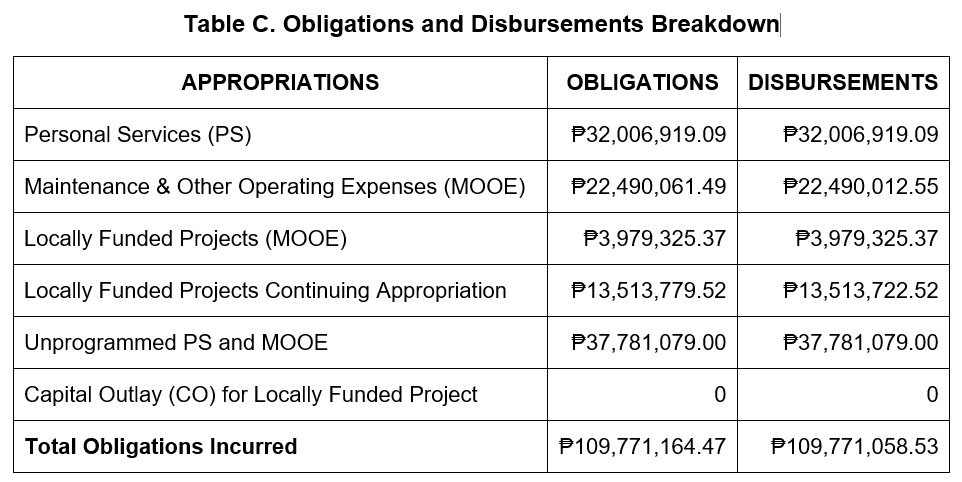

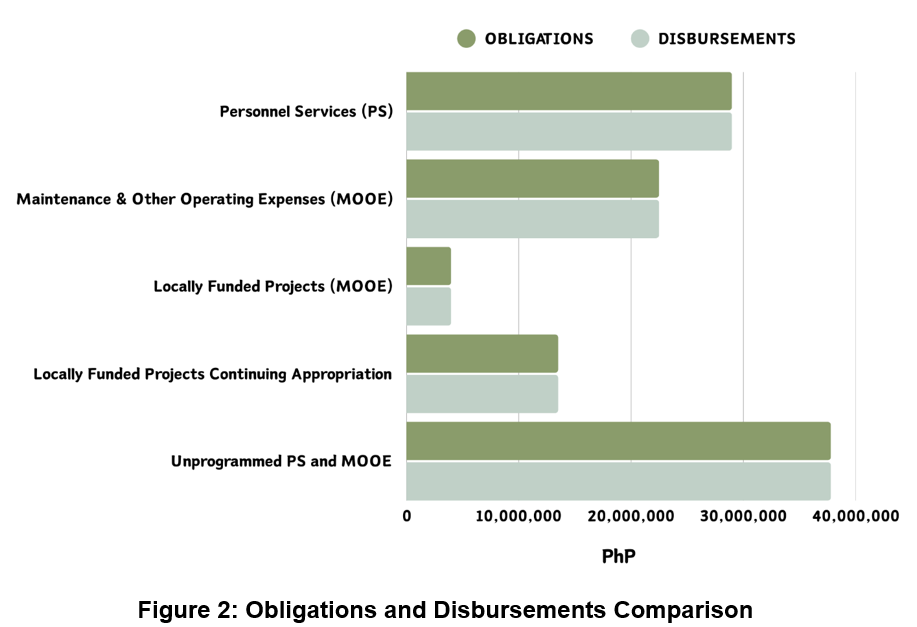

In summary, the total obligation paid by PSA RSSO IV-A as of March 2025 amounts to PhP109,771,164.47 and an actual disbursement amounting to PhP109,771,058.53, reflects the total amount spent by the regional office. This spending is likely distributed across various categories such as Personnel Services, Maintenance and Other Operating expenses, and funding for other programs, activities and projects. The breakdown is essential for understanding the allocation of resources and ensuring that the budget is being used efficiently to carry out administrative and statistical operations (refer to Table C and Figure 2).

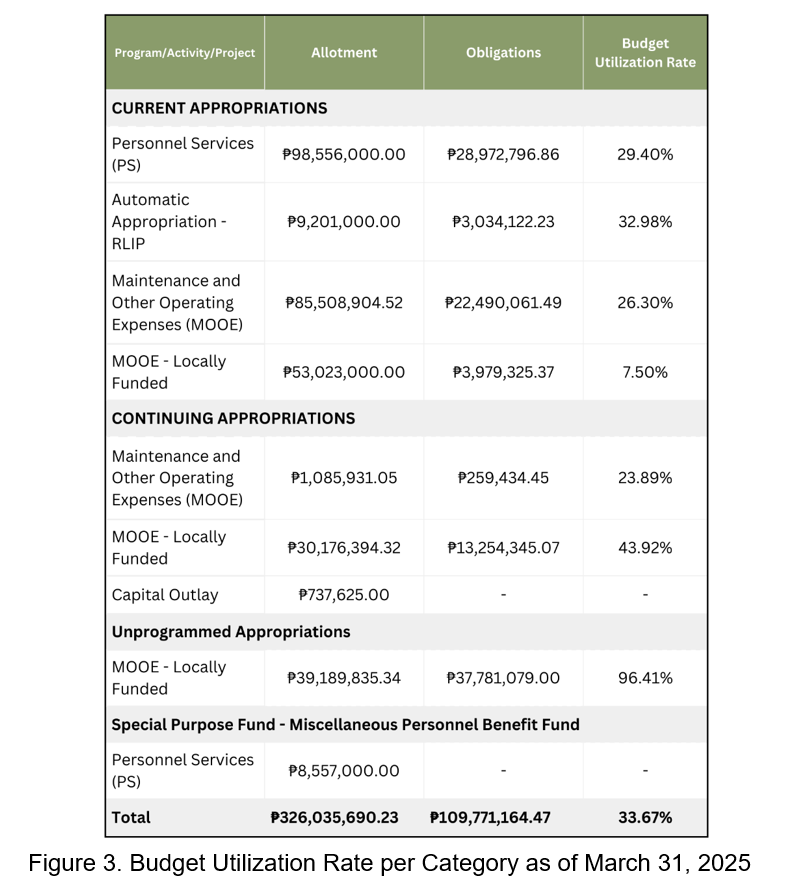

The Budget Utilization Rate (BUR) is a key metric used to measure how effectively an organization or agency is using the allocated budget within a given period. It is computed by dividing the total obligations over total appropriations. The average utilization rate of CALABARZON for the period January – March 2025 for the given period was 33.67%, with three (3) more quarters to fully utilize the allocated resources. The utilization rates for different categories are as follows:

1. Regular Program Personnel Services (PS): 27.52% of the allocated budget for Personal Services (such as salaries, wages, and benefits for employees) has been utilized.

2. Regular Program Maintenance and Other Operating Expenses (MOOE): 26.30% of the budget for MOOE (expenses such as office supplies, utilities, travel expenses, etc.) has been spent.

3. Regular Program Maintenance and Other Operating Expenses (MOOE) – Continuing Appropriations: This category reflects the utilization of funds allocated to MOOE under locally funded projects, with a low utilization rate 23.89% at the end of first quarter.

4. Locally Funded Projects MOOE – Continuing Appropriations: The 43.92% utilization rate for Continuing MOOE for locally funded projects suggests that, while a significant portion of the allocated budget has been used, the 56.08% unutilized portion due to ongoing project, activities and programs still be used until the 4th quarter of 2025.

5. Unprogrammed MOOE: A 96.41% utilization rate for unprogrammed funds for MOOE shows that the organization has been using the available funds effectively to cover unforeseen expenses related to operational costs.

6. Locally Funded Projects Capital Outlay: This shows a 0% utilization rate for capital outlay in locally funded projects, meaning that no funds have been spent so far, or no expenses have been incurred on capital expenses like infrastructure, equipment, or long-term investments for these projects. This indicate that capital expenses have not yet been incurred. This will be obligated and disbursed by the month of April for the procurement of aircon unit for the 2024 Census of Population and CBMS Data Processing.

7. Personnel Services Special Purpose Fund – Miscellaneous Personnel Benefit Fund (MPBF): This shows also a 0% utilization rate for MPBF, meaning no expenses have been incurred for this quarter. This will be obligated in this coming 2nd quarter of the year.

Overall, the utilization rates across various categories are still low, except for Unprogrammed – MOOE, since the allotted resources will be used up until December 2025.

(SGD.)

CHARITO C. ARMONIA

Regional Director

WAV/ACF

| Attachment | Size |

|---|---|

|

|

3.17 MB |

Reference Period

2025